Yesterday, we discussed how the SmartCity concession gradually transformed from a promised ICT hub into a speculative real-estate project financed through shareholder support, related-party funding and eventually public bond markets. We also discussed how Kevin Deguara and his associate Jean-Carl Farrugia acquired the shares of the project for free and that today, despite rounds of financing, the project, called Shoreline Mall is still financially distressed.

The issue is even more convoluted, and the financial structure even more distressed than it appears prima facie, as the complex financial layering behind the project reveals that the “related-party funding” was itself being financed through the public bond market. Beneath all of this lies an underlying reality suggesting that Kevin Deguara and Jean Carl Farrugia never had sufficient independent capital to finance their involvement in the project themselves, with their funding instead relying on a convoluted and opaque layering structure intertwined with money raised from the public markets.

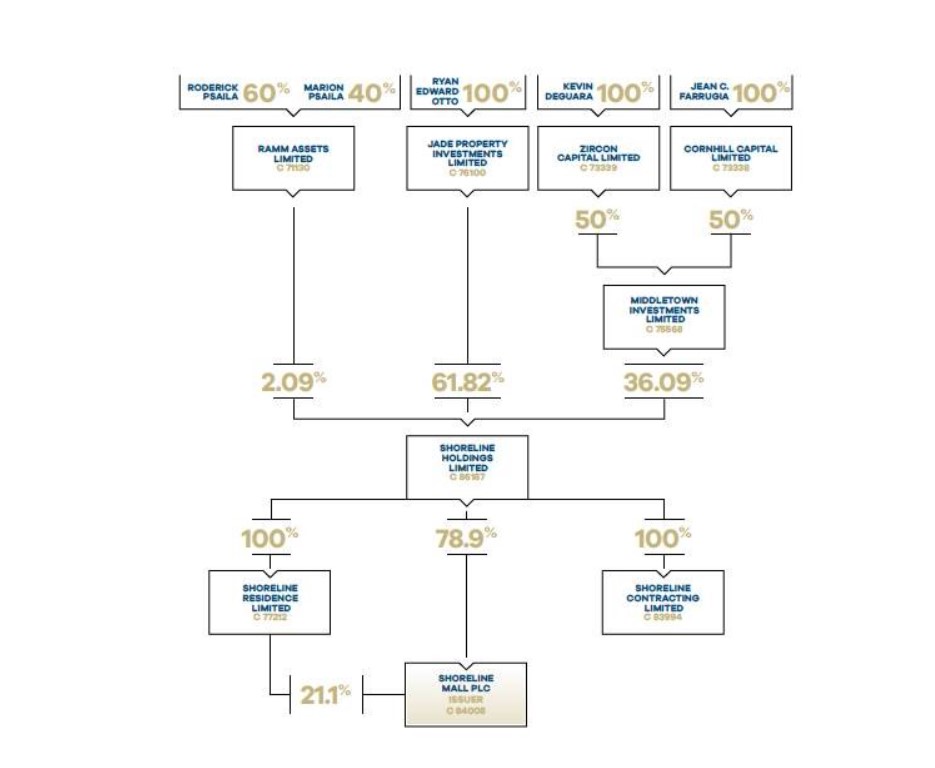

Kevin Deguara and Jean-Carl Farrugia own their stake in Shoreline Mall via Middletown Investments which is owned by Zircon Capital Ltd and Cornhill Capital Ltd. The public filings of Middletown Investments show that bond investors in Horizon Finance may have indirectly financed the Shoreline project through a network of intra-group loans and related-party financing arrangements.

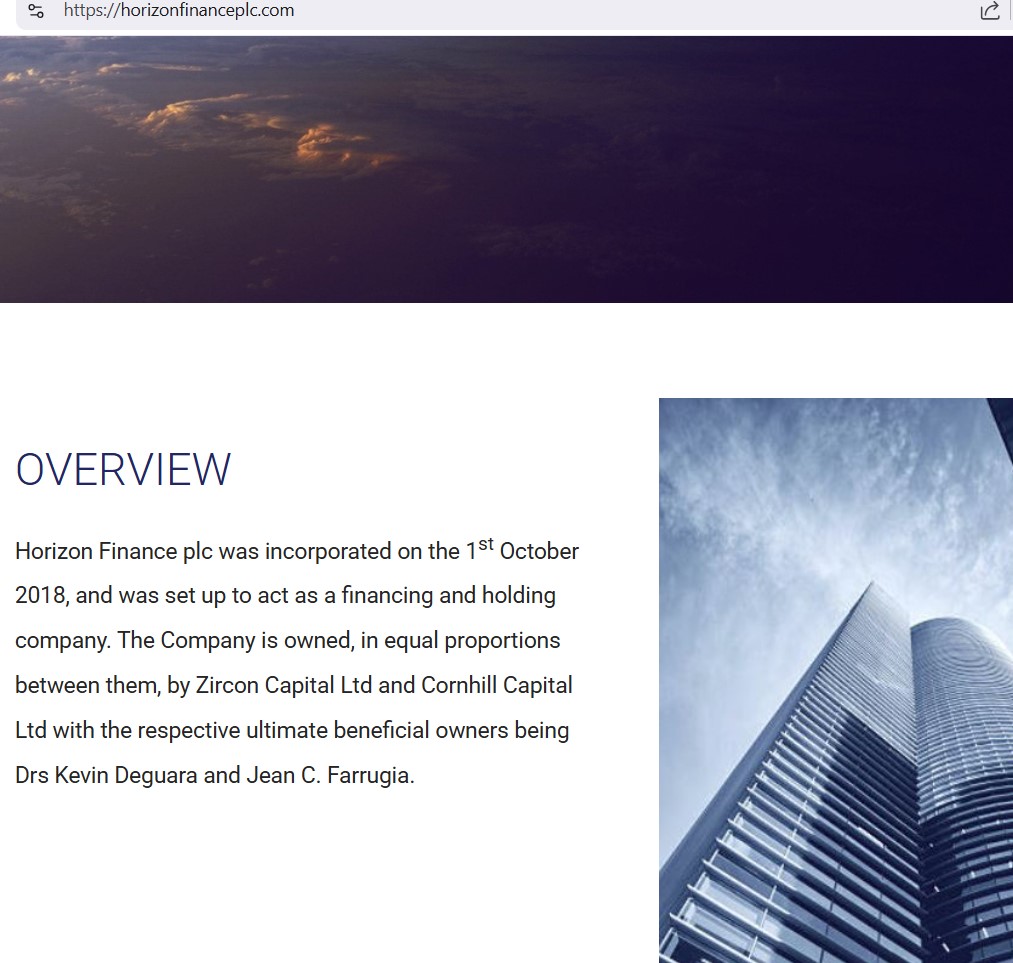

Middletown’s own audited accounts describe Horizon Finance not as an independent operating business, but specifically as a financing vehicle created to “carry on the business of financing or refinancing of the funding requirements of the Company and the Group.” The “Company and Group” in question is Middletown Investments Limited and its associated companies. Middletown itself acts primarily as a holding and investment company. Its financial statements explicitly state that its purpose includes lending money, granting guarantees and providing financing to companies forming part of the same group.

Strangely enough, this is part of the financing structure is not being fully disclosed to the Shoreline investors.

In its 2023 financial statements, Middletown disclosed that it had an outstanding loan of €850,000 from Horizon Finance plc carrying interest at 7.25% and repayable by February 2029. At the same time, Middletown reported more than €1.26 million in loans receivable from associates.

One of Middletown’s principal associates is Shoreline Holdings Limited, the SmartCity-linked real-estate structure in which Middletown held approximately 36.09% by 2024.

The pattern becomes increasingly difficult to dismiss as coincidence.

Middletown’s loan from Horizon Finance carried long-term financing terms and a 7.25% coupon. Meanwhile, Middletown steadily increased its loans advanced to associates from €862,000 in 2022 to €1.262 million in 2023 and over €1.7 million by 2024.

The accounts do not explicitly state that these loans were advanced directly to Shoreline Holdings.

The broader financing chain strongly suggests that funds raised through Horizon Finance ultimately circulated into the Shoreline ecosystem through Middletown Investments.

The group’s consolidated balance sheet also indicates the same.

Middletown’s 2024 consolidated accounts disclose approximately €1.97 million in debt securities in issue together with extensive related-party borrowing arrangements.

Those debt securities correspond to the bond financing structure operated through Horizon Finance.

The result is a layered funding model in which:

- Horizon Finance raises money through publicly listed debt,

- Horizon finances Middletown,

- Middletown advances loans into associated companies,

- and Shoreline sits among those associated real-estate structures.

In practical terms, this means that Maltese retail investors purchasing Horizon Finance have indirectly financed Shoreline Mall without necessarily realising how deeply interconnected the structures were.

This came on top of Shoreline Mall’s own direct bond financing.

Shoreline Mall plc itself issued €14 million in 4% secured bonds maturing in 2026 and another €26 million in 4.5% secured bonds maturing in 2032 in order to sustain construction and liquidity pressures. Shoreline can’t guarantee that it will fulfill its upcoming bond payments.

Middletown Investments is not generating any value or actual profits and it’s use is simply as a financial vehicle to funnel capital to Shoreline via its interconnected and layered web of companies and associated individuals. In accounting terms, Middletown’s own profits depended heavily on fair-value gains (property) rather than operating cashflow. The company recorded €1.18 million in fair-value gains in 2023 and another €604,057 in 2024.

The broader picture now emerging from the filings is that the Shoreline project was financed by a complex network of related-party financing arrangements supported by public bond markets and layered through interconnected companies. The result is that the Maltese public has financed the same distressed real-estate ecosystem multiple times over through overlapping debt structures tied to Shoreline Mall, Horizon Finance and Middletown Investments.

Website Editor

Historian and Publisher

Leave a Reply