Digging deeper into the financing structure of Shoreline Mall, the red flags keep mounting as the combined nature of the accounts gives the impression of a textbook government-backed real-estate grift built on layered financing structures. Shoreline Mall plc’s bonds are distressed, with no guarantee that bond payments will be made, while the company appears dependent on highly opaque financing structures to support its debt obligations.

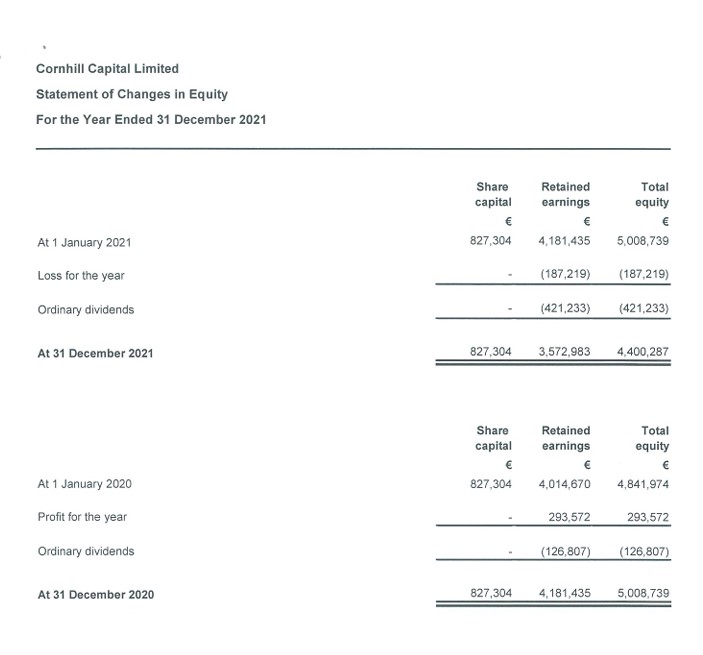

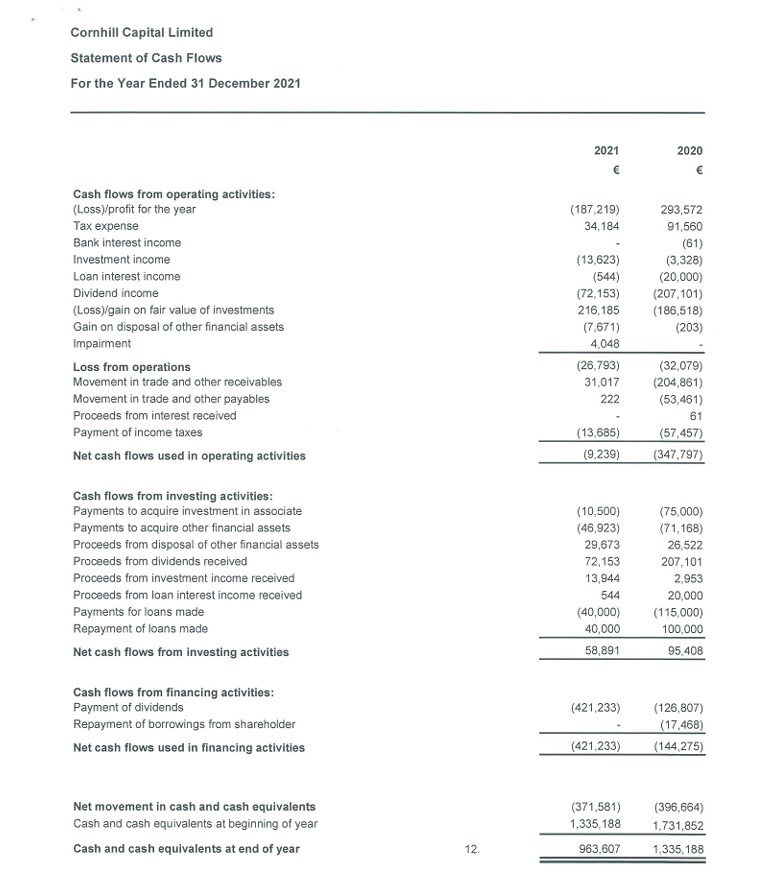

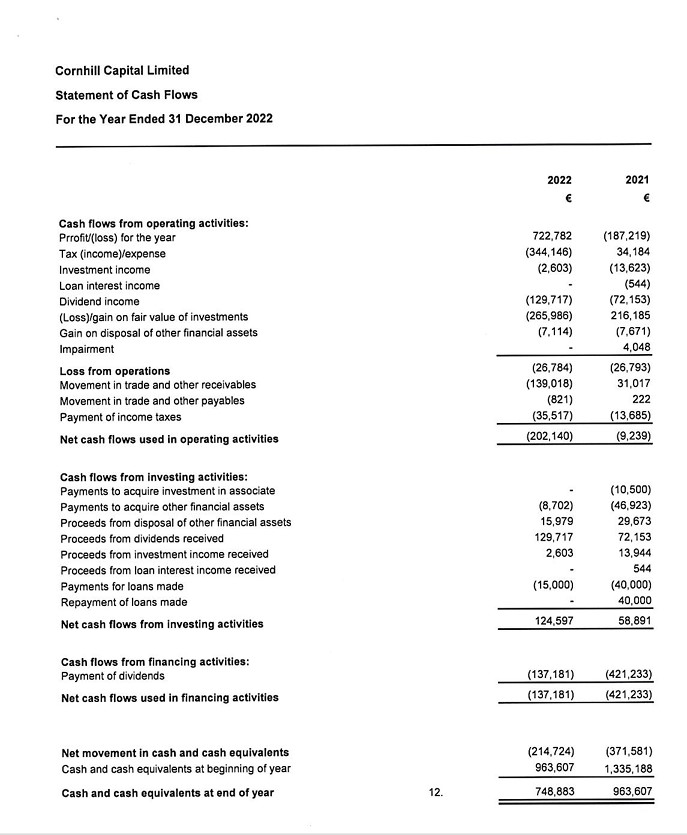

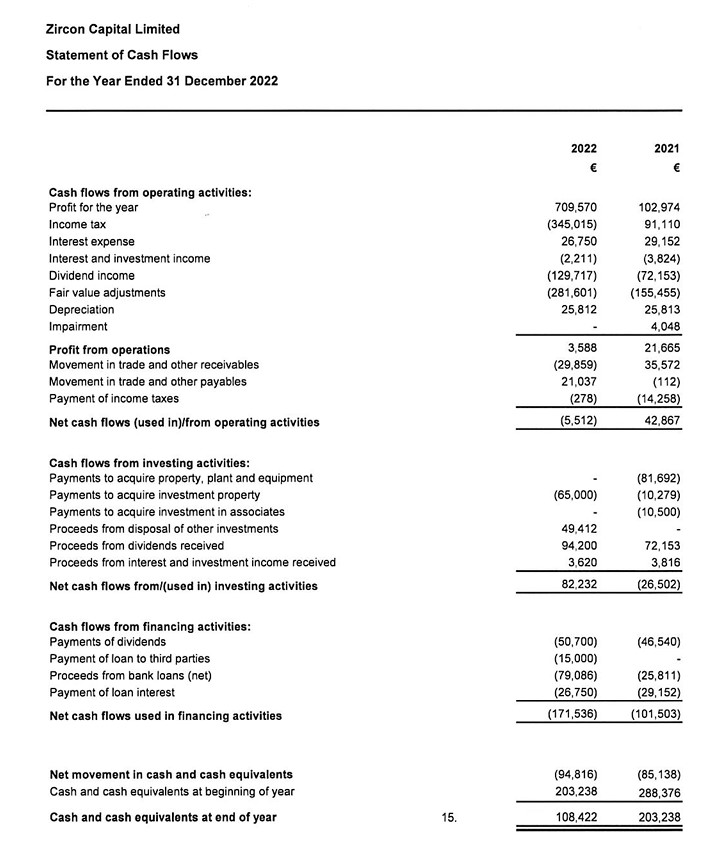

Despite the main asset remaining financially stressed — the company owning the shopping mall at Kalkara’s ex-SmartCity site — companies owned by Kevin Deguara and Jean Carl Farrugia continued registering profits while Shoreline Mall itself was making losses and burning cash throughout its development phase. The profits were registered by Zircon Capital and Cornhill Capital, which jointly own Middletown Investments. Middletown itself also registered profits and ultimately holds the Shoreline stake linked to Kevin Deguara and Jean Carl Farrugia.

Shoreline Mall itself remained heavily indebted, dependent on public bond financing and vulnerable to recurring losses. The combined accounts show that value is being pushed higher up the chain in the companies structures through associate profits, fair-value gains, related-party loans and dividends, effectively obscuring the underlying nature of the large financial flows taking place within the structure.

The structure itself is crucial to understanding the arrangement. Zircon Capital and Cornhill Capital jointly control Middletown Investments. Middletown in turn owns 36.09% of Shoreline Holdings Limited (the combined stake of Deguara and Farrugia), the real-estate holding company connected to the Shoreline project. Middletown’s 2024 accounts confirm that Shoreline Holdings is one of its main associates, alongside Phoenix Capital and GAIA Investments.

Middletown’s role is not passive. Its stated activity is to own and manage property interests, lend and advance money, provide credit and grant security to companies within the same group. Its subsidiary, Horizon Finance plc, is explicitly described as the financing vehicle used to finance or refinance the funding requirements of Middletown and the group. Yet the Shoreline financing structure and related prospectuses did not clearly disclose the full extent of this interconnected financing arrangement.

The first unusual correlation appears in 2022. Zircon Capital recorded a profit of €709,570 and paid €50,700 in dividends, while Cornhill Capital recorded a profit of €722,782 and paid €137,181 in dividends. Both companies held Middletown as part of their associate portfolio.

In the same year, Middletown itself recorded a profit of €803,893. However, that profit was not generated through ordinary operations or productive business activity. Middletown’s cash-flow statement shows that once fair-value gains and other non-cash accounting adjustments are stripped out, the company was effectively loss-making from operations. Its 2022 profit included a fair-value gain of €156,728 and other income amounting to €320,000.

The following year, the pattern became even more pronounced. Middletown’s 2023 profit rose to €1.29 million, but this was overwhelmingly driven by a €1.18 million gain on the fair value of investments. The company also received €180,484 in dividend income while continuing to report negative operating cash flow.

Meanwhile, Shoreline Mall itself was not producing the type of operating performance that would normally justify upstream profit-taking or dividend extraction. Shoreline’s 2023 financial year showed a loss of €401,412 while construction and development costs remained ongoing. In 2024, Shoreline reported a profit of €1.19 million, but this was largely driven by the sale of car park assets to a related party during the same year rather than by recurring operational profitability.

By 2025, Shoreline Mall had returned to losses. The company generated €2.98 million in rental income and €2.37 million in net rental income, but after administrative expenses and €1.74 million in finance costs, it posted a €1.68 million loss before tax. Almost all finance costs stemmed directly from bond interest, with €1.73 million in interest expense on debt securities alone.

This is the central contradiction within the structure: Shoreline itself was losing money and paying substantial bond interest, while Middletown, Zircon and Cornhill were simultaneously able to register profits through associate accounting, valuations and financial engineering. The accounting structure effectively obscures the underlying movement of value and cash within the wider group.

Middletown’s investment in associates rose from €5.1 million in 2022 to €6.29 million in 2023 and €6.88 million in 2024. In its consolidated accounts, Middletown recorded a share of profit from equity-accounted investments amounting to €2.13 million in 2023 and €591,221 in 2024. In its standalone accounts, these movements appear primarily as fair-value gains.

At the same time, Middletown was advancing loans to associates. Loans receivable from associates rose from €862,000 in 2022 to €1.26 million in 2023 and €1.76 million in 2024. One of these loans carries a 7.25% interest rate and is repayable in 2029 — mirroring the same interest rate and maturity profile as financing Middletown itself received from Horizon Finance.

The accounts strongly suggest the existence of a circular financing structure: Horizon Finance raises or channels financing into Middletown; Middletown lends money to associates; Shoreline sits within that associate structure; and the value of those associates then supports profits, valuations and accounting gains higher up the chain.

The 2025 and 2026 forecasts make the structure appear weaker rather than stronger. Middletown’s forecasts show a €1.14 million loss in 2025 and a further projected loss of €279,170 in 2026. The company is also forecast to continue carrying approximately €1.97 million in debt securities, €2.44 million in current borrowings and an additional €250,000 loan expected to be advanced to an associate in 2026.

Shoreline itself remained heavily exposed to group-company balances. Its 2025 accounts show €16.1 million due to group companies, down from €22.4 million in 2024. The accounts explicitly state that Shoreline Contracting Limited entered into agreements directly with contractors for the development and construction of the Shoreline Mall project and that these costs were financed through group companies.

The result is a deeply layered structure in which public bondholders financed the operating company at the bottom, while related-party vehicles higher up the chain potentially extracted value through associate profits, valuations, loans and dividends.

Zircon and Cornhill cannot yet be conclusively said to have directly siphoned cash from Shoreline Mall on the basis of the currently available accounts alone. However, the accounts do show that they benefited from a structure in which Shoreline’s underlying project was financed through public bonds and group debt, while upstream vehicles were simultaneously recording profits and distributing dividends during periods in which Shoreline itself was either loss-making, still under construction or dependent on continuing related-party financial support.

That remains the major red flag. The profits registered by Zircon and Cornhill do not appear to originate from conventional operating businesses generating stable productive cash flow. Instead, they appear heavily linked to the valuation and associate-accounting chain built around Middletown Investments, whose most important real-estate associate remained Shoreline Holdings.

Website Editor

Historian and Publisher

Leave a Reply