The chart of the stock price of Malita Investments looks like a slow train-wreck in the process. Unsurprisingly, the board has notable supports of the Labour Party including the ex-Chief Risk Officer who approved of a €36 million loan to Steward Health Care Malta. Current works by Malita Investments have been stalled and the Social Housing Minister Rodrick Galdes is facing calls for resignation over a corrupt property purchase he made from a one of the social housing contractors.

Other Labour Party supports in the board include Victor Carachi (also GWU), Desiree Cassar and Tania Brown. the new chairman of the public company is Marvin Gaerty – the corrupt ex taxman. The CEO, Jennifer Falzon, resigned at the end of last year and was paid a salary of up to €90,000 every year. She resigned over the scandal in which the Social Housing Minister was accused of fraudulently placing the ID Card residence of his supports in a social housing block in Siġġiewi, in his electoral district.

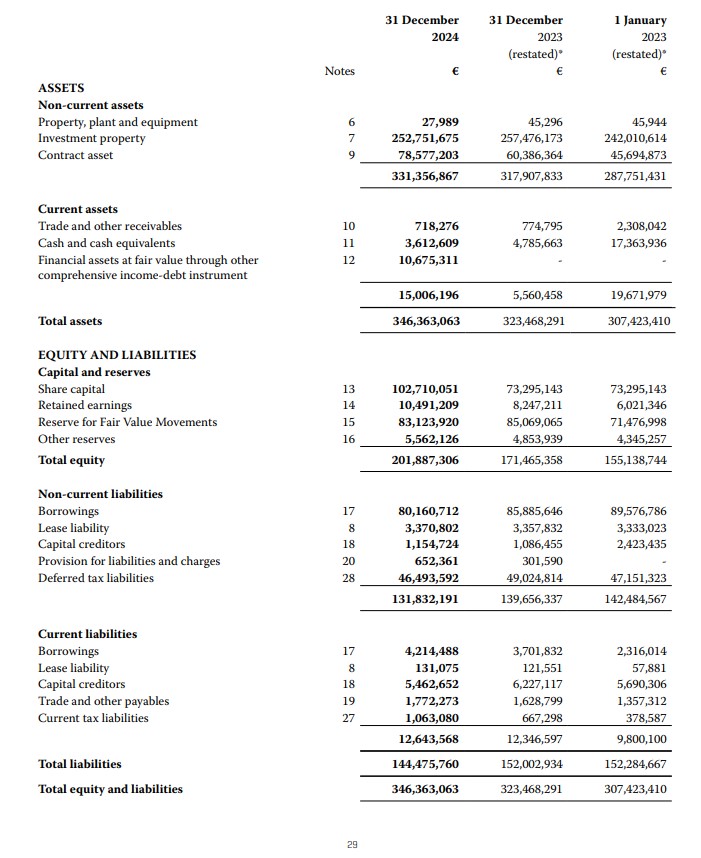

According to its annual report, by the end of 2024 its debt to equity ratio jumped from 41.8% to 52.2% while declaring a slight increase in operational profit of €8.77 million, up from €8.32 million. The increase in debt to equity ratio indicates the company was taking loans to fund its projects. The company is indebted by up to €90 million with most of the debt being non-current (payable in the years to come). Debt however looks to have decreased slightly in 2024 according to its income statement. On the other hand, actual profit for 2024 was around €6 million, considerably less than 2023 of up to €19.69 million.

The company states that it has to up to €252 million in investment property and up to €78.57 million in contract assets.

The numbers of the company make sense for a company that is currently investing in social housing as a social principle but clearly the company does not seem to be positioned to offer any value to shareholders. The company is only profitable because it can sustain its projects by debt but as soon as the company runs out of projects to implement, it will run out of its ability to raise debt, eventually facing with a large credit bill.

The problem with Malita Investments is that it was originally just a government holding company of some of its properties including its remaining equity at the Malta International Airport and the Valletta Cruise Port. Mixing in with this holding company the concept of social housing would have supposedly gone against the original mandate of Malita Investments. In addition, social housing projects should have never been commercialised via public company on the stock exchange.

Today, Malita Investments has a liquidity problem and that is why essentially ongoing projects have stopped. The government has to invent many creative ways to get the company’s stock price back on track but the problem is that the government doesn’t even have an incentive to do this given to how the company has been structured. The company can keep taking on loans for social housing projects that it can build both on public and private land which is what the government is mostly interested. The incumbent Social Housing Minister has probably exacerbated a very messy situation in the company with his corruption, unraveling its inherent structural problems.

Website Editor

Historian and Publisher

Leave a Reply